From Budgeting to Automation: Top Online Loan Repayment Strategies You Need to Know

Mon, 03/18/2024

We feel you, luv. Paying off debt can be overwhelming and stressful, especially if you're dealing with multiple loans. We know how hard it can be to keep up with due dates and varying loan amounts. But we can’t just give up on it, right? Thankfully, there are now online lending platforms that provide borrowers with access to a wide range of tools and strategies to make loan repayment more manageable.

From something as simple as budgeting to more complex ideas like loan consolidation, refinancing, and automation, here are some of the top online loan repayment strategies you need to know!

TOC

If you have a loan at the very least you have to know how much you owe, when you have to pay it back, and how the interest rate adds up to the total amount. A quick way to find out is by logging into your online loan account and taking note of these details.

On top of that, it’s also important to know the minimum payment required for each loan. This allows you to organize your debt and make repayments much easier. In addition to loans, don’t forget to pay back your credit cards since they usually have higher interest rates.

Don’t feel bad if all this information is overwhelming, luv. You can always look at online loan calculators to help you better understand your loans.

Related: Personal to Business: A Complete Guide to Online Loan Types & Alternatives TOC

We know, preparing a monthly budget isn’t a load of fun, but it’s guaranteed to help you keep your finances in check.

Many people create spreadsheets for their monthly budgets. If Microsoft Excel isn’t your forte, you can always try one of the many user-friendly budgeting apps available for your smartphone.

Once you’ve found the app that’s perfect for you, you can divide your expenses into different buckets like groceries, food, leisure, and – of course - loans. Using your previous months’ expenses as reference, you can then place a reasonable amount for each bucket.

If you’re still dreading the idea of creating a monthly budget for your loans, just keep telling yourself that this is only temporary, and that you can delete that app or spreadsheet once you complete repayment. Or who knows, maybe you’ll get used to budgeting. After all, it’s one of the many ways you can maintain a financially independent life.

TOC

Missed loan repayment dates can lead to late fees and/or increased interest rates, which could then end up damaging your credit score. Who cares about my credit score? Uh-oh, hun! Think twice about that and read up more on the importance of keeping a healthy credit score here. If you’ve set up alarms for repayment and that still doesn’t work, then maybe it’s time to turn to automation.

Automatic loan payments automatically deduct the amount from your bank account on the due date so you don’t have to remember when to make said payments. This can also help you avoid spending the money that’s supposed to be for loan payments.

TOC

It can be tempting to pay just the minimum amount per month since you’ll be able to pay off your debt while still having more money to spend. However, it’s better to practice delayed gratification and pay more than the minimum amount. That way, you’ll be able to fully repay your loan earlier, and you’ll save up on interest.

Before you do this, though, make sure to check the terms of your loan in case there are any additional fees or prepayment penalties.

TOC

Some borrowers opt for bi-weekly payments to shorten the life of their loans, but that strategy feels too demanding for others. If that’s how you feel, then you can instead make one extra payment per year. This one little extra change can help make a big difference, especially if you use a tax refund or a bonus at work to pay.

If you want to lessen the pain of repayments even more, you can also distribute the amount of that one extra payment across 12 months of the year. Now you’ll hard feel its impact. However, please note that not all loans allow this set up. Some loans are more flexible than others.

TOC

When you make payments for loans, a large chunk of the amount goes towards interest, not the amount that you borrowed. Because of that, it’s best that you get those high-interest loans out of the way as quickly as possible.

Following the tip we shared earlier, pay more than the minimum amount for the loan with the highest interest, then pay only the minimum for the rest. Once you’ve paid that loan off, do the same thing for the next loan with the highest interest. Rinse and repeat.

TOC

In this method, you start by paying off the loan with the smallest balance, then make your way up to the loan with the biggest balance – sort of like a snowball that’s rolling down the hill, gradually getting bigger. This strategy is great for building momentum as you pay off all your debts.

TOC

This is easier said than done, but this is one of the most straightforward ways of getting the extra cash to pay back your loans. Instead of relying on your day job, you can start a side hustle during the weekends. Got a bunch of random stuff at home that you don’t need anymore? Go ahead and sell them on any of the many e-commerce platforms at your fingertips!

TOC

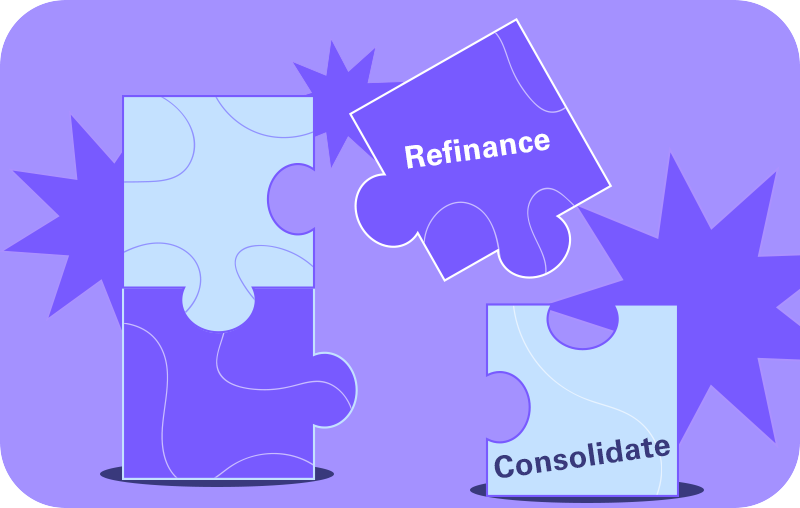

Simply put, refinancing means taking out a new loan with a lower interest rate to pay back a current loan. On the other hand, loans for debt consolidation are loans used for the purpose of paying back existing multiple loans. Ideally, the amount of this new loan should be equal to the combined balance of your existing loans, but with a lower interest rate.

TOC

After exploring refinancing and consolidation as ways to manage your loan repayments more effectively, another strategy worth considering is debt restructuring. Debt restructuring involves negotiating with your lenders to modify the terms of your loans, potentially lowering your interest rates, reducing monthly payments, or extending the repayment period.

By restructuring your debt, you can avoid the consequences of missed payments, such as damaged credit scores and late fees, and keep your repayment plan on track.

TOC

If you’re feeling overwhelmed by the amount of loans you must pay back, then don’t add more to your portfolio – simple as that! This includes other debts like credit card bills. Instead, switch to using cash or swiping that debit card instead. You’ll be less tempted to overspend, forcing you to make wiser money decisions.

TOCYes, it is possible to negotiate the repayment terms of your online loan. But this will depend on the lender's policies and your specific situation. Contact your lender and explain your current circumstances. It’s worth a shot.

If you have tons of online loans to pay, then refinancing or debt consolidation is a great way to manage online loan repayments. Through refinancing or debt, you don’t need to worry about missing payment deadlines and paying late fees.

But keep in mind that refinancing and consolidation are two different terms. Know the difference to understand what you’re getting yourself into.

As they say, prevention is infinitely better than cure. If you want to avoid defaulting on your online loan repayments, it’s best that you do not borrow more than you can pay.

But if you already have an existing loan, then just make timely payments and you’ll be good to go.

Unfortunately, you’ll be slapped with late fees and interest charges. And if you let it go on for too long, it may negatively impact your credit score. Your lender might even take legal action against you. Talk to your lender to negotiate a way for you to pay them back.

It depends on your loan’s fine print. If your lender allows extra payments, then why not? But if they don’t, they may allow you to pay your loan in full instead. You may be able to save more in terms of time and interest this way.

If you miss a payment on your online loan, it is important to contact your lender as soon as possible to explain the situation and ask about options for catching up on missed payments. You may be able to negotiate a payment plan or deferment.

First, check your loan provider’s website or app if they’re capable of setting automatic loan repayments. You’ll then have to provide your bank account information plus the frequency and amount of your payments. Once that’s done, your loan payments should be deducted automatically from your bank account on the due date.

List all your sources of income, then categorize your expenses. Prioritize your loan payments, but don’t forget to set aside some money for emergencies. Remember to review your budget regularly, too, and adjust whenever needed.

This largely depends on your personal financial situation and goals. Additional factors to consider include the interest rate, the loan amount, repayment period, your income, and your expenses. Make sure to assess your options and choose a strategy that best fits your budget and priorities.

The loan repayment period varies, and it largely depends on factors like the loan amount and interest rate. Note that longer repayment periods will typically have lower monthly payments but higher interest, while shorter repayment periods mostly mean higher monthly payments but less interest.

The first thing you should do is to confirm with the lender if your account has been closed and if the loan has indeed been paid in full. Then, check your credit report to see if the loan has been marked as "paid." Finally, if you still have some of that money that you've been using to pay back the loan, you can set it aside for emergencies or your savings.