So, you’re thinking about borrowing money but the sound of the word “loans” even as you begin to utter it, scares the life out of you. Don’t worry too much since loans aren’t that daunting. Here are the ways and tips you can loan in the Philippines so you can choose the best one suited for you!

Loans—it sounds like a small word, sure, but it’s a big adult thing that you might have to go through should the situation for it arise, such as emergencies you probably won’t expect (pesky wisdom tooth extractions, sickness in the family, etc.) or life opportunities that you know you don’t want to miss out on (getting into a top university, taking post-graduate studies abroad, starting a business, etc.)!

At first, it might be quite scary, but loans really don’t have to be a huge ordeal, as long as you know where the right resources are, and which terms are the best ones for you. We got you all covered through this tell-all blog, so sit tight and let us walk you through the best ways to borrow money in the Philippines!

Editor’s Pick

Before we get into it all, perhaps you’d like to ask us and us alone: what’s the ONE best way to borrow money in the Philippines, anyway? While “best” could be subjective, we’d like to weigh in that technology in finance has been gaining more and more traction over the past few years, making not just banking easier, but loaning as well! So, for us, finance apps and similar digital platforms (like us, Tonik!) would be the best way to do it in these modern times.

Why? Because it’s super easy to get—you only need around 2 documents (usually your valid ID and a document that proves consistent income), no collaterals, and a verified account on your app of choice! And when you use an app for loans, application and disbursement only take minutes! No more long lines and waiting time, terrifying loan sharks, and risky business. With Tonik, you can try out our Credit Builder Loan or our Shop Installment Loan.

Okay, now onto the nitty-gritty...

Table of Contents

- Lending apps and platforms

- Installment Loans and Buy Now Pay Later programs

- P2P Lending

- Credit Card Cash Advance

- Pawnshops

- What are the requirements for Credit Builder Loans and Online Loans in the Philippines?

- How much is the minimum/maximum amount you can borrow from lending institutions in the Philippines?

- How long does it take to get finance approved? And how long does it take to get the money?

- What is the minimum/maximum term duration of Credit Builder loans in the Philippines?

What is a Loan?

You might not be aware of it, but you’ve probably borrowed money at least once in your life, even if it’s a small amount. In fact, as much as 47.1% of Filipino adults borrow money as of April 2023. So, you might already know what a loan is! Basically, a loan is the act of lending money by individuals, financial institutions, organizations, or groups, to another party.

Usually, the repayment of a loan involves interest along with the actual amount that is borrowed. Loans may also involve collateral, which usually comes in the form of a property title or valuables that prove to the loan firm that you are good for the loan you are taking out, and terms of the loan must be agreed upon by both parties (borrower and lender) before any money is disbursed or given.

TOC- Table FIndTypes of Loans in the Philippines

There are a lot of loans you can get in the Philippines! Here are the 5 common types:

- Personal Loan – These are a type of unsecured loan (meaning: no collateral) that you can use for almost anything under the sun, like paying for your bills, starting a business, paying tuition fees, and the like. A lot of institutions offer personal loans, from banks to fintech apps. The terms normally vary along with how much you can actually borrow. Banks usually have a more rigid approval process versus digital platforms. More on this later!

- Emergency Loan – These are fast loans that you can get in times of trouble, such as calamities. The emergency loan is popular with Filipinos who have little to no income or credit history which isn’t the best, because most of the time, private lenders for emergency loans only require valid IDs. Application and disbursement are also usually very quick, but with interest rates that are super high, like 1% to 1.5% per day levels of pricey! Government agencies like SSS and Pag-IBIG offer Calamity Loans to those living in high calamity areas, too.

- Home Loan – A home loan is something people get when they want to purchase property, like a house or a condo! The lender (for example, a bank or Pag-IBIG) will have the rights to your property as collateral until the loan has been fully paid. The terms for this can be as long as 30 years and as short as 5 years.

- Car Loan – This loan uses the vehicle you want to buy as collateral, since the lender or organization you are loaning from will have the rights to your car throughout the duration of the loan. The terms for a car loan may last around 3-5 years.

- Buy Now, Pay Later Loan – These are used for shopping purposes and are available with partners at department stores or apps like Home Credit and us, Tonik! Shopee and Lazada have BNPL programs as well. You use these loans when you want to buy something bigger than usual, such as a gadget, appliance, etc.

The Pros and Cons of Getting Personal Loans

Pros of a Personal Loan:

- You can use it for (mostly) anything – Whether those are just for bills, travel, tuition fees, etc., the personal loan is quite flexible and versatile! They’re called “personal” for a reason, right? A lot of financial organizations let their borrowers use the money for different purposes. Obviously, you can’t do anything illegal with a personal loan. Duh!

- You can build your credit score with it – If this is your first-time loaning, then this will be a good start to building your credit score should you make the payments on time.

- It’s fast – This depends on where you get your loan from, but there are lots of online private lenders that offer personal loans super quick. Application and approval won’t take a week or more, like your regular bank loans. Tonik offers personal loans with application and approval in just 30 minutes!

- No need for collateral – Personal loans are normally unsecured, so you don’t need to offer anything valuable up (like a car, land title, or jewelry) for collateral.

- Flexible terms – Because personal loans can vary per borrower, that means terms can be super flexible as well, from a wide range of loan amounts to installments. You won’t be pressured to pay right away. For example, Tonik’s Credit Builder Loan allows you to borrow for up to Php 20,000, with installment terms from 6-12 months.

Cons of a Personal Loan:

- Interest rates are typically high – If you get an unsecured personal loan, then your interest rates would probably be higher versus a personal loan that would require collateral.

- It could come with penalties and late fees – Be careful when it comes to looking for companies to get a personal loan from because the terms could have various fees that they’d use for processing. If you pay late though or have insufficient funds, be ready to be charged with penalty fees. Other financial organizations charge prepayment penalty, too. It’s the fee you pay for paying the loan too early, although lots of lenders no longer have this. Always look at the loan terms.

- You could get a bad credit score – In the case that you don’t pay your loan diligently or on time, then this could hurt your credit score as well. So, it’s a two-way situation when it comes to your credit score. You can either build it up or bring it down. Be very careful when it comes to paying on time, luv!

- It can lead to unnecessary debt if not handled correctly – Self-explanatory. Be responsible when you loan.

Wanna know more about personal loans? You could check out our article on different personal loan myths being busted right here.

TOC

TOC

Cheapest Ways to Borrow Money in the Philippines

TOCBanks

Traditional banks are most likely the first option you’d think about when looking for a loan—after all, they’re one of the most trusted financial/lending institutions around. It’s safe and usually top of mind for most consumers and companies when it comes to financing. But while they do give affordable loans, it isn’t easy to qualify for one. More on this here:

Pros of Bank Loans:

- Low interest rates – Banks are among the institutions able to offer low interest rates due to their high standards for loan approvals and meticulous processes. If you’re one of the lucky few to get one, you can enjoy this for yourself.

- Predictable monthly payment – Banks also usually offer fixed payments so you’ll know what you’ll be paying for every month. At least this way, you’d be able to budget better and have good foresight when it comes to your expenses.

- Helps build credit – One good thing about getting a loan with a traditional bank is that it builds credit history, especially when you pay your dues on time. Again, it could go the other way if you don’t, so make sure you always pay on schedule.

Cons of Bank Loans:

- Lots of paperwork required for application – The application process for banks is quite lengthy, and a lot of requirements would be needed. This also normally involves multiple bank visits and going face to face with bank employees and personally submitting everything to them. It might be a little bit of a hassle for some borrowers.

- Long processing time – Processing could also take days and sometimes weeks because some traditional banks do manual, often meticulous checks before approving a loan.

- Need for collateral – Bank loans often require collateral, which is why interest rates offered are low. Not too good for those with no assets or with issues using their assets for this purpose.

- Need for good credit history – You normally need some form of credit history to get a bank loan, so if you’re a first-timer, you can kiss this option goodbye.

Government Loans

These loans come from various government agencies, ideal for those looking for loans of small amounts with interest rates that aren’t unreasonable. After all, government loans were created to protect citizens from high-interest rates. Different government agencies such as SSS, Pag-IBIG, CHED, and more have different programs that cater to different purposes, like housing, education, etc. Here are some examples:

-

TOC

-

Pag-IBIG Multi-purpose Loan

- This is a loan that allows Pag-IBIG to assist its members with financial needs. A Pag-IBIG member is able to borrow up to 80% of their savings with this institution. Plus, they claim to have quicker processing than other government loans—2 days total!

TOC

-

SSS Salary Loan

- This is also a benefit of SSS members doing regular contributions, and borrowers can use it for their short-term financial needs. The amount would depend on your contributions to SSS as well. Because of their fast approval process and low interest rates, this type of loan is quite popular with 29 billion pesos disbursed to around 1 million members in 2019 alone. Wow!

Pros of Government Loans:

- You normally don’t need credit history to apply – Therefore, this loan is easy to get! Minimal documents are needed as well.

- Low interest rates – This is why government loans are widely used as well, because they offer among the lowest interest rates compared to private lenders or banks.

Cons of Government Loans:

- The amount you can get is limited – Government loans are limited, sadly, and most of the time, you can only borrow an amount that you’ve contributed. So, this loan is best for people in search for amounts that aren’t too huge.

- Long approval times – Processing takes some time with government loans. The fastest you can get a loan would probably be a couple of days, which isn’t great for someone who’d need money fast.

- You need to meet certain criteria of the institution or be a member – With agencies like SSS and Pag-IBIG, you’d need to be a member to avail of their loans.

Collateral Loans

Collateral Loans are a type of secured loan where you pledge an asset such as a car or your property as collateral while taking out a loan. You basically borrow some money but also exchange something of value that the lender will be keeping until the debt is paid. Popular collateral loans are offered by companies like AsiaLink Finance and traditional banks such as Security Bank, Metrobank, BDO, and others.

Pros of Collateral Loans:

- Easy approval – Since your loan is secured by a collateral, approval would be easier and more guaranteed as compared to unsecured loans. Yass!

- Higher loan amounts – Someone trying for a collateral loan can apply for a big amount based on the value of their asset. There’s no max amount that can be loaned.

- Lower interest rates – Again, this is because your loan is secured by collateral, so interest rates would be low as well.

Cons of Collateral Loans:

- You need collateral – Of course, you can’t take out a collateral loan if you don’t have anything of value! If you do, you need to be okay having something valuable of yours be offered as collateral. If you don’t, then maybe other loan options are better for you.

And take note, if you’re planning to take out another loan, you can only use a particular collateral once.

Cooperatives

Cooperatives are also known as credit unions. These are financial institutions similar to banks, except they are owned by the customers themselves and exist for their benefit as well. They do not exist for profit, compared to banks. There are varying types of cooperatives that are there for different purposes, such as for agriculture, housing, health, and many others. Cooperatives are obliged to follow their specific purpose and they also offer different financial products like home loans, student loans, auto loans, etc.

Pros of Cooperatives:

- You’re part of the community – Credit unions involve membership, so ideally, you would be a member with dividends and benefits.

- Low interest rates – Most cooperatives in the Philippines offer around 1-2% interest monthly compared to the more expensive rates given by online platforms and digital banks.

- Good customer service – Because this is a smaller organization, there is more room to be customer-oriented and friendly, so you can expect better customer service from being a part of a cooperative.

- Easy application and flexible plans – Some of these cooperatives operate online so application would also be hassle-free and there are many installment terms that cater to its members.

Cons of Cooperatives:

- You need to pay a membership fee – Of course, to become a member of a cooperative, you must first pay a membership or subscription fee. This would also vary according to the cooperative you choose.

TOC

Fastest Ways to Borrow Money in the Philippines

TOCLending apps and platforms

Online loans and lending apps are another easier alternative to borrowing money in the Philippines, since around 70-80% of Filipinos are unable to loan through banks due to lack of credit history. Private online loans and lending apps are borrowing methods that operate digitally, through websites or apps.

Compared to bank loans that have high qualifications and a lengthy process, lending apps typically only require a valid ID and proof of income, making it a lot more convenient for those who have no experience with traditional banks. Examples of lending apps include Cashalo, Tala, Tonik (of course!), Digido, and a lot more!

Pros of Lending Apps:

- Convenient, easy application – As mentioned earlier, application is fuss-free and these companies only require minimal documents. This, however, would vary per lending company. Make sure to check the requirements of the online loan you choose to get!

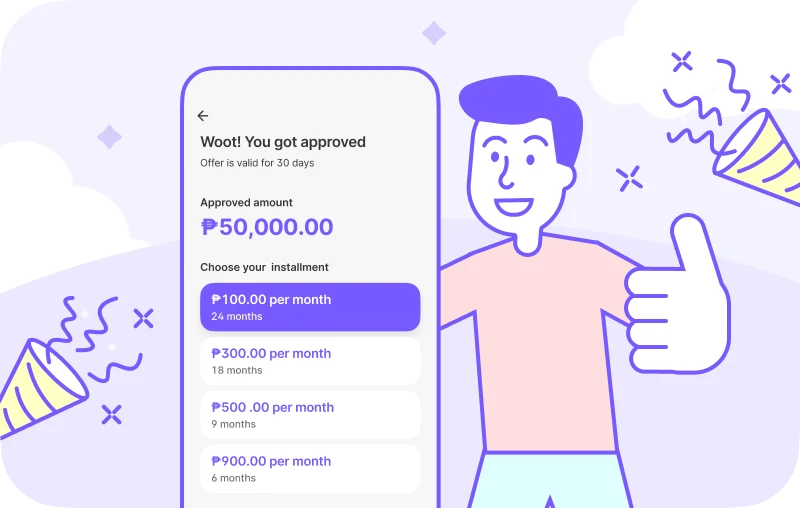

- Fast disbursement – If the application takes a day or even less, then disbursement is even faster! Tonik, for example, disburses the loan instantly to your Tonik Savings Account after the 30 minutes that it takes you to apply (this is for Credit Builder Loan, FYI).

- Apply anytime, anywhere – Because these platforms operate digitally, you can apply at whatever time you want and anywhere! Just open your app or website of choice. No more lining up at banks or submitting documents personally. It’s the age of tech, baby!

Cons of Lending Apps:

- Short terms – Since you can borrow very low amounts of money at a time from these apps (Tala offers loans as low at Php 1000), terms are also normally shorter as well, with some that last only a month or so. For Tonik, the shortest loan duration for Credit Builder Loan is 6 months.

- High interest rates – Because you don’t need credit history or many requirements, plus application is a breeze, interest rates are normally higher than what you’d see from traditional loans. These are typically unsecured loans without collateral, so it’d be more expensive to pay back.

- Possibility of scam – Because it’s online and you may not get to meet anyone in real life for your loans, there’s always the possibility of getting scammed out of your money. Make sure to only borrow from verified online lending companies that have reviews from actual people. Do your research and stay vigilant when dealing with finance digitally. Lots of scammers might even claim to be associated with legit companies—remember that you do online loans by yourself and with no third parties!

Installment Loans and Buy Now Pay Later programs

These loans, more known as BNPL programs, help customers buy appliances, gadgets, or other items online or in-store and allow them to pay on a later date or in installments—hence the name “buy now, pay later.” This lets consumers purchase things instantly should they need them but not have enough funds to do so.

Home Credit is among the most popular companies that offer BNPL loans. Tonik also has one called Shop Installment Loan, with presence in stores such as Home Along.

Pros of BNPL:

- 0% interest – There are BNPL offers that don’t offer any more interest, making it more convenient than paying via credit card.

- Instant gratification – You want it? You got it! When you choose a BNPL loan or program, then you can immediately get that item you’ve been eyeing! It’d be a win especially if it’s an appliance or gadget that you need.

- Long loan terms – There are BNPL installment terms that can go as long as 24 months. With Tonik, you choose the loan duration that you’re comfortable with, and we’re flexible like that!

- Offline presence – Apart from shopping online, BNPL companies have presence in appliance stores, and you can use apps like Home Credit, Grab Pay, Zip, or Tonik to buy something from there. Just open your app to get the loan and use it as a mode of payment. Other stores also have their own BNPL programs that you can try out.

Cons of BNPL:

- Interest rates – Some BNPL programs don’t offer 0% installments, so you’ll end up paying more than the actual price of the item you purchased. The interest rates vary per lending company.

- The impulse to keep shopping/buying – Because of the choice to “pay later,” you may be tempted to just keep on shopping even if you don't have enough savings. Remember, you’d be spending money you don’t have, so this option might just tempt you to keep buying things, and therefore incurring even more debt. Try to manage your impulses when taking out BNPL loans.

- Transaction or late fees – Again, you might be spending more than you intended due to transaction or processing fees when you take out a BNPL loan or program. Also, if you pay late, you may be penalized with more fees just like a regular loan.

P2P Lending

This is short for “Peer to Peer” lending, meaning you loan from actual individuals and peers instead of a financial institution, like a bank. You get the loans from a pool of money from investors (sometimes, even just one investor). An example of a P2P lending platform is Blend.ph, where you can both borrow or invest. It’s a little like how a mutual fund works.

Pros of P2P Lending:

- Fast application – It's similar to online loans and application is done online, so they’re also more convenient to apply for.

- No need for collateral – These P2P loans are unsecure, so you don’t need collateral for it.

- Credit checks aren’t strict – There is still checking of credit history involved to gauge a borrower’s capability to repay, but they aren’t as strict as compared to banks or other traditional companies.

Cons of P2P Lending:

- No insurance – If you’re a lender, your money isn’t insured and can potentially be lost to borrowers with bad credit scores. You also do not have government protection.

- Additional fees – If you’re a borrower, there may be additional fees to your loan added apart from the interest rates, like processing charges.

Credit Card Cash Advance

The perks of having a credit card is not just you being able to pay for expenses with it, but also being allowed to get a cash advance from it via an ATM. It’s not the same as withdrawing from your debit card because that involves money from your bank account. A credit card cash advance is essentially borrowing from your credit limit.

Pros of Credit Card Cash Advance:

- Extremely fast and instant – As mentioned, you just have to use your credit card to withdraw at your nearest ATM. Boom, instant cash! It’s easy and quick.

- No application process – Because all you need to do is go to an ATM to withdraw money using your credit card, then there’s no application process to go through or documents to show.

Cons of Credit Card Cash Advance:

- High interest rates – With great, instant money comes great responsibility, including—you guessed it—high interest rates. Credit card cash advances are expensive because it immediately starts getting interest the moment you withdraw, so you should settle your credit card bills ASAP or earlier to avoid paying too much.

- Can lead to bad credit score – If you try and get a credit card cash advance, then this may potentially hurt your credit score, since lending companies see people who frequently use credit card advances as irresponsible and unlikely to pay their debts.

- Extra fees – Aside from interest rates, you would also need to pay more fees when you get your cash advance, depending on how much you will withdraw. It normally would cost around a certain percentage of that. This varies from bank to bank.

- The temptation to keep getting it – Because it’s so easy to get a credit card cash advance, you might be tempted to withdraw again and again. Pro tip: if it’s starting to affect your finances, then just don’t!

- You need a credit card – Obviously, you can’t get a credit cash advance without having a credit card! You would have to go through the credit card application to try this, which is also a hassle in itself, considering all the credit checks and documents to submit.

TOC

Pawnshops

There are loads of pawn shops in the Philippines and that’s because it allows people to get money the easy way. All they need to do is hand over a valuable object as collateral to the pawn shop, whether it’s an expensive piece of jewelry, a gadget, a luxury item, a car, land title, etc. The shop will then give you a loan should they accept your valuable.

Pros of Pawnshops:

- Accessible and fast – Again, there are many pawn shops in the country, some of which are open 24/7 for emergencies if you need cash ASAP. All you need to do is to bring your collateral at the nearby pawn shop, with no more hassles.

- No need for credit history – This is another reason why Filipinos go to pawnshops for loans, because there is no need for background checks or applications. You hand over your collateral and you settle on the date you come back for it as well as the value that you can pawn it for. Plus, pawnshops don’t report their customers’ credit to the authorities, so you don’t risk your credit history being dirtied.

- Licensed pawnshops – The BSP regulates pawn shops, so make sure that the one you go to is BSP-supervised! You can sleep well knowing that because of this, the shop won’t run away with your collateral as the BSP ensures that business in pawn shops is ethical and legal.

Cons of Pawnshops:

- Your collateral may not be returned, or it could break – This is the risk that comes with pawnshops. You wouldn’t want this to happen especially if the valuable you used as collateral is a family heirloom, for example. Or if it’s a laptop that you need for work. It could also possibly be damaged while in the possession of a pawnshop. You never really know how safe your collateral is.

- High interest rates – Similar to online loans, because it’s so easy to process, the interest rates are normally higher, typically around 3-4% per month. Licensed pawn shops such as Cebuana Lhuillier, M Lhuillier, Tambunting Pawnshop, and other big names offer this interest monthly.

- Low prices – Pawn shops are known for lending at low prices, so don’t expect to get the full value of your collateral. You can expect to get maybe half the price, if ever.

TOC

Lending and borrowing options to avoid in the Philippines

- Borrowing from friends and family – Don’t lie—we’ve all borrowed from friends or family at some point in our lives, whether it’s a small amount of money easily payable in just a day or two or a huge amount that probably would’ve been better to find elsewhere. We get it.

It’s extremely tempting to borrow from your loved ones because there would likely be no interest, no installment terms, and no collateral involved. And of course, there’s no complicated application needed! Just ask and you will receive; they’re family after all! They’re supposed to have your back in times of trouble, right?

While this sounds great at first, you can’t deny that a lot of drama comes up when your loans with your loved ones go wrong. Perhaps you’ve even experienced it if you borrowed from a close friend or family member. There’d be a lot of gossip, arguments, and fights if ever you would not be able to pay them back on time, or even at all!

They’re our loved ones for a reason. While borrowing cash from them might seem convenient at first, you don’t want to lose their trust or ruin relationships because of something as worldly as money. Treat your loved ones and their hard-earned savings or salary with respect, and try to avoid loaning from them if it involves a gigantic amount of money. - Payday loans – These are unsecured instant loans that you can normally get easily and of course, fast. The catch is, you must pay the due during your next payday, hence its namesake. There is usually an additional fee when you apply for these loans as well. Try to avoid this since apart from the fact that interest rates are high, this would also be an easy way to accumulate debt since you’re essentially spending money you don’t have. Before you know it, you could be drowning in dues because of all these instant loans.

- Loan sharks – Just don’t even think about this one! Loan sharks are notorious for having insanely high-interest rates for their loans, and when you miss a payment, they could resort to violence or terrifying threats that are just not worth the money you’ll be borrowing—not to mention that you won’t have terms written on paper or a record of repayments, making everything very messy and hard for you to track your debt. Don’t fall for their traps as you really wouldn’t like a lifetime of harassment if you don’t get to pay them back.

- High-interest loans – Examples of high-interest loans (both of which are illegal, FYI) include 5-6 lending and Sangla ATM. These are typically the schemes involved with loan sharks. 5-6 loans have interest rates that can go as high as 20%, while Sangla ATM loans have lower interest rates but would ask the borrower to turn over their ATM card as collateral. This would then leave the borrower highly vulnerable to things like fraud, identity theft, scams, and other nasty occurrences. Plus, the lender may also withdraw more than what the borrower actually loaned.

TOC

Tips for getting your loan application approved in the Philippines

- Clean your credit score – A high credit score is normally needed to get a loan. If you have an existing credit score, make sure it’s good enough by getting on top of your existing debts, such as credit card dues, and always pay on time! If you don’t have credit history, don’t worry, because there are lots of private lenders and digital banks that don’t require it for applications, like Tonik!

- Borrow only what you need – We know it's super tempting to just go for the biggest amount, don’t forget, this is a commitment. You’ll need to pay it back eventually. So, think about it: how much do you really need to borrow? If you're looking at an amount that’s too huge and lenders see that you don’t really have the capacity to pay back your dues, then your application will most likely be rejected. Only loan what you can afford.

- Find the lender suited to your situation – First time borrower with no credit score? Then a traditional bank loan won’t be for you; try online lenders instead, since they’re more lenient with applications. Are you a student on the hunt for a student loan? Try the government loan from CHED! When hunting for a loan, you have to make sure the lender’s terms are suited to your situation and your needs. Are you employed or not? Are you looking for an emergency loan? Do you want to buy a gadget? These are questions you need to ask yourself because there are loans and lenders out there that cater to what you need. All you’ve got to do is assess and search.

- Have a steady source of income – Most of the time, financial organizations that offer loans will ask you for proof of income. If you’re a salaried employee, then that’s a good step in ensuring an approved loan. Lending institutions will usually ask for your most recent pay slips to make sure you can pay off debts.

- Keep a good balance in your bank – In relation to the last bit, private lenders will ask you to submit one or the other: your latest pay slip or your latest bank statement. To prove your financial capacity, have enough savings in your bank and make sure you regularly place funds there.

- Prepare all documents needed – If you’re loaning from a traditional bank, then they’ll probably be asking for a lot of documents for their paperwork. Get those already beforehand so that you’re ready for it. Government errands can take a while. On the other hand, if you loan from online lenders or digital banks like Tonik, you’ll only need a valid government ID. For that, ensure that your ID isn’t expired at the very least!

- Make sure all information is accurate – When you’re filling up a loan application form, triple check your information because you may be declined should your details be erroneous. Your information should add up to all of your supporting documents so look at your application thoroughly before passing it to your desired lender.

TOC

Tips for paying off debt

- Have a budget – To make sure you don’t spend too much and still have enough money to pay all your dues, make sure to keep a handy weekly or monthly budget. Set aside all your bills and dues and put them on your budget so that you know how much you need to pay for every month, as well as the rest of your expenses. This makes sure that you manage your money wisely and don’t spend blindly. Not sure how to make a budget? Why not try a money management app to make your life easier?

- Pay more than the minimum balance, if possible – If your loan terms allow it, try paying more than the minimum balance every month so that you can save your interest. The goal is to pay off your loan quicker than usual. But make sure you check on your terms again before you do it, because some lending companies impose prepayment penalty.

- Find ways to earn extra money – If you have the time and resources to work extra, then by all means, do it if it involves earning some more cash! There are lots of easy ways to earn money online, with websites like Upwork and Fiverr, requiring various skills that may fall under your skillset! Time to hustle!

- Consolidate debts – In a nutshell, debt consolidation is combining multiple debts into one and turning them into a single payment. A number of traditional banks in the Philippines offer this, including BDO and Citi. This allows you to at least organize your debts and pay a fixed payment per month instead of chasing multiple dues that might be confusing.

- Target one debt at a time – If you don’t have the option of consolidating debts, you can try targeting one at a time: either the most expensive debt, or the smallest one! Targeting the most expensive debt (called debt avalanche) allows you to save a bit more in the long term while handling cheaper debts (called debt snowball) would be easier and less pressuring. It all depends on what you can handle and what strategy you choose.

TOC

Credit Builder Loans in the Philippines FAQs

-

TOC

- What are the requirements for Credit Builder Loans and Online Loans in the Philippines?

Not a lot, actually! This is one of the pros of online loans in the country—you don’t need many requirements to apply for one. Normally, online lending platforms such as Tonik, will only ask for a valid government ID and either your latest pay slip or your latest bank statement, and of course, a verified account on the app. Other online lending platforms vary, but most of the time, you just have to be 18 and older and have a valid ID.

-

TOC

- How much is the minimum/maximum amount you can borrow from lending institutions in the Philippines?

It really depends on the lending institution that you go for, luv! For example, some companies like Tala can loan for as low as Php 1000 and as high as Php 50,000. Usually, these are low amounts that can be paid back in a short amount of time. If we’re talking about Tonik’s Credit Builder Loans over here, then the minimum loan amount would be Php 5000 and the highest would be Php 50,000—the normal range for fast online loans. On the other hand, Tonik’s Shop Installment Loan maximum amount is Php 100,000.

-

TOC

- How long does it take to get finance approved? And how long does it take to get the money?

They’re called Credit Builder loans for a reason, luv! For Tonik’s Credit Builder Loan, you can apply and get approved in just 30 minutes maximum (even faster if you’ve got fast fingers and prepared all your documents beforehand), with cash disbursement to your Tonik Account happening soon after in just seconds. Other lenders such as Tala would take 24 hours for application to be approved—still pretty fast compared to your traditional banks.

-

TOC

- What is the minimum/maximum term duration of Credit Builder loans in the Philippines?

Because online loans are for the short term, the minimum duration would usually be 2 weeks at the shortest and 2 years (24 months) at the longest! At Tonik, our Credit Builder Loan’s shortest term is 6 months and its longest is 12 months, with other installment periods in between for the customer to choose from.

Still spooked about taking out a loan? No? That’s awesome! We told you that it’s not so difficult or taxing. The best thing to do is to always do your research and truly understand which one is the best loan for you. There’s one out there for everybody—whether it’s someone with no credit history, someone in need of quick cash for an emergency, and the like! All you need to do is look, hun! If you’re not sure where to start, Tonik’s got some awesome loans for you to look up right here.

Sources:

- Pautang in the Philippines: Where to Borrow for Emergencies

- What are the Common Types of Loans in the Philippines? | Coins.ph

- Most Common Types Of Loans In The Philippines

- Pros And Cons Of Personal Loans – Forbes Advisor

- The Pros and Cons of Student, Personal, and Government Loans | Bukas

- Local Business Funding: Pros and Cons of Bank Loans and Private Financing

- Bank Loans for Small Business Financing: Pros & Cons | Nav

- 14 Easy Ways to Pay Off Debt | US News

- Boost Your Chances of Getting Your Personal Loan Approved - NerdWallet

- How to Fight Loan Shark Harassment in the Philippines

- Five Reasons to Avoid Instant Payday Loans - Credit Counselling Society.

- Online Lending vs. Banks: A Guide to Business Loans in the Philippines - First Circle

- Payday Loans in the Philippines up to 30 000PHP for you | Best opportunity - Golden Peso

- Online Loans Philippines 24/7 - Only Need ID Card

- Cooperatives in the Philippines

- Legit Online Loan Apps in the Philippines: What are the Options?

- Buy Now, Pay Later in the Philippines: What is It and How Does It Work?

- Peer-to-Peer (P2P) Lending Definition

- How to Invest in Peer-to-Peer Lending in the Philippines [Complete Guide]

- Collateral Loans & Financing Philippines | Asialink Finance

- Collateral loans in the Philippines: how to use? Apple online

- Credit Card Cash Advance in the Philippines: Is the Risk Worth It?